Sustainability and agrifood sectors fuel Singapore startup growth

![]()

The verticals closed 16 and 13 deals, respectively, in 2023.

7 hours ago

Sustainability and agrifood sectors fuel Singapore startup growth

The verticals closed 16 and 13 deals, respectively, in 2023.

7 hours ago

8 out of 10 Singaporean Millennials and Gen Zs prefer off-peak travel

67% believe they can accomplish more during these quieter periods.

12 minutes ago

CapitaLand India Trust's net property income surges 18% YoY in 1Q24

The REIT attributed the increase to higher property income.

1 hour ago

Suntec REIT's distributable income dips 1.1% YoY in 1Q24

With lower income, the REIT also reported a 1.8% dip in DPU.

1 hour ago

Condo resale prices increase by 5.0 YoY in March

Across submarkets, OCR posted the highest year-on-year price increase.

1 hour ago

Condo resale volume jumps 17.4% MoM in March

Over 800 units got resold during the month.

1 hour ago

Singapore properties boost OUE Commercial REIT’s NPI by 6.9% YoY

These properties include Hilton Singapore Orchard.

1 hour ago

Keppel's net profit rises in 1Q24, fueled by key sectors

With legacy offshore and marine assets factored in, net profit dipped YoY.

1 hour ago

FCT's net property income declines 8.4% YoY amidst asset changes

With lower NPI, FCT also recorded a decline in its DPU.

1 hour ago

Singapore SMEs’ cyber risk awareness declines: report

Fewer SMEs were affected by cyber events this year.

7 hours ago

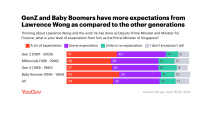

Incoming PM Wong garners broad confidence across all age groups

Gen Zs (41%) and Baby Boomers (43%) hold high expectations for Wong.

7 hours ago

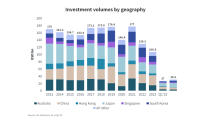

Singapore, APAC commercial real estate investments up in Q1

Singapore property investments hit US$2.2b last quarter.

7 hours ago

StanChart joins Visa’s B2B Connect to enhance cross-border payments

It aims to facilitate faster and more cost-effective business-to-business (B2B).

21 hours ago

DCS Card Centre, E6 launch credit card issuing solution for fintechs

The service will be first rolled out in Singapore.

21 hours ago

SINGAUTO secures $61.2m funding for global expansion plans

The company will begin mass production of the S1 new energy cold chain vehicle to deliver over 20,000 units by 2025.

23 hours ago

BRC Asia buys 19.1% stake in Angkasa for $16.1M

Post acquisition, BRC will own a 19.1% stake in Angkasa.

23 hours ago

BRC Asia buys 19.1% stake in Angkasa for $16.1M

23 hours ago

Highlights

Highlights

Partner Content

Partner Content

Exclusives

Exclusives

Financial Services

Industry boosts accounting appeal with new roles, education programmes

There has been a 10% decrease in accounting degree students at universities in Singapore.

Commercial Property

Colliers transforms Singapore office into regional powerhouse

![Colliers transforms Singapore office into regional powerhouse]()

![Colliers transforms Singapore office into regional powerhouse]()

The newly revamped office showcases Colliers’ commitment to innovation, collaboration, and sustainability.

Markets & Investing

Days of excess are over, investors warn founders

![Days of excess are over, investors warn founders]()

![Days of excess are over, investors warn founders]()

Deal activity in Asia Pacific fell 26.3% YoY in 2023.

Markets & Investing

Sustainability, biomedical startups draw investors, founder focus

![Sustainability, biomedical startups draw investors, founder focus]()

![Sustainability, biomedical startups draw investors, founder focus]()

A nine-month study in 2023 showed green tech investments totalling $268.5m (US$201m).

HR & Education

MBA offerings refined amidst downturn in enrollment

![MBA offerings refined amidst downturn in enrollment]()

![MBA offerings refined amidst downturn in enrollment]()

Despite adaptation to post pandemic shifts and the elevated value of MBA degrees, enrollees drop 8.3% in 2023.

HR & Education

Singapore's plan to raise retirement age sparks debate

![Singapore's plan to raise retirement age sparks debate]()

![Singapore's plan to raise retirement age sparks debate]()

Experts see Singapore on track to setting retirement at 65 and re-employment at 70 by 2030.

Advertise

Advertise

Top News

Sustainability and agrifood sectors fuel Singapore startup growth

![]()

The verticals closed 16 and 13 deals, respectively, in 2023.

7 hours ago

Sustainability and agrifood sectors fuel Singapore startup growth

The verticals closed 16 and 13 deals, respectively, in 2023.

7 hours ago

8 out of 10 Singaporean Millennials and Gen Zs prefer off-peak travel

67% believe they can accomplish more during these quieter periods.

12 minutes ago

CapitaLand India Trust's net property income surges 18% YoY in 1Q24

The REIT attributed the increase to higher property income.

1 hour ago

Suntec REIT's distributable income dips 1.1% YoY in 1Q24

With lower income, the REIT also reported a 1.8% dip in DPU.

1 hour ago

Condo resale prices increase by 5.0 YoY in March

Across submarkets, OCR posted the highest year-on-year price increase.

1 hour ago

Condo resale volume jumps 17.4% MoM in March

Over 800 units got resold during the month.

1 hour ago

Singapore properties boost OUE Commercial REIT’s NPI by 6.9% YoY

These properties include Hilton Singapore Orchard.

1 hour ago

Keppel's net profit rises in 1Q24, fueled by key sectors

With legacy offshore and marine assets factored in, net profit dipped YoY.

1 hour ago

FCT's net property income declines 8.4% YoY amidst asset changes

With lower NPI, FCT also recorded a decline in its DPU.

1 hour ago

Singapore SMEs’ cyber risk awareness declines: report

Fewer SMEs were affected by cyber events this year.

7 hours ago

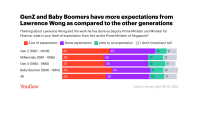

Incoming PM Wong garners broad confidence across all age groups

Gen Zs (41%) and Baby Boomers (43%) hold high expectations for Wong.

7 hours ago

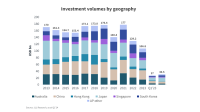

Singapore, APAC commercial real estate investments up in Q1

Singapore property investments hit US$2.2b last quarter.

7 hours ago

StanChart joins Visa’s B2B Connect to enhance cross-border payments

It aims to facilitate faster and more cost-effective business-to-business (B2B).

21 hours ago

DCS Card Centre, E6 launch credit card issuing solution for fintechs

The service will be first rolled out in Singapore.

21 hours ago

SINGAUTO secures $61.2m funding for global expansion plans

The company will begin mass production of the S1 new energy cold chain vehicle to deliver over 20,000 units by 2025.

23 hours ago

BRC Asia buys 19.1% stake in Angkasa for $16.1M

Post acquisition, BRC will own a 19.1% stake in Angkasa.

23 hours ago

BRC Asia buys 19.1% stake in Angkasa for $16.1M

23 hours ago

Partner Content

Partner Content

Highlights

Highlights

Exclusives

Financial Services

Industry boosts accounting appeal with new roles, education programmes

There has been a 10% decrease in accounting degree students at universities in Singapore.

Commercial Property

Colliers transforms Singapore office into regional powerhouse

![Colliers transforms Singapore office into regional powerhouse]()

![Colliers transforms Singapore office into regional powerhouse]()

The newly revamped office showcases Colliers’ commitment to innovation, collaboration, and sustainability.

Markets & Investing

Days of excess are over, investors warn founders

![Days of excess are over, investors warn founders]()

![Days of excess are over, investors warn founders]()

Deal activity in Asia Pacific fell 26.3% YoY in 2023.

Markets & Investing

Sustainability, biomedical startups draw investors, founder focus

![Sustainability, biomedical startups draw investors, founder focus]()

![Sustainability, biomedical startups draw investors, founder focus]()

A nine-month study in 2023 showed green tech investments totalling $268.5m (US$201m).

HR & Education

MBA offerings refined amidst downturn in enrollment

![MBA offerings refined amidst downturn in enrollment]()

![MBA offerings refined amidst downturn in enrollment]()

Despite adaptation to post pandemic shifts and the elevated value of MBA degrees, enrollees drop 8.3% in 2023.

HR & Education

Singapore's plan to raise retirement age sparks debate

![Singapore's plan to raise retirement age sparks debate]()

![Singapore's plan to raise retirement age sparks debate]()

Experts see Singapore on track to setting retirement at 65 and re-employment at 70 by 2030.

Event News

Event News

Cladtek Holdings secures win at SBR National Business Awards 2024

![Cladtek Holdings secures win at SBR National Business Awards 2024]() Co-Written / Partner

Co-Written / Partner

Its iN-Shield initiative is built on the 9 competencies with the best practices on the market that optimises the processes.

Its iN-Shield initiative is built on the 9 competencies with the best practices on the market that optimises the processes.

Commentary

AI is revolutionising learning: Why should educational institutions in Singapore embrace this change?

Seeking an office space in Singapore: Where do you start?